HELPING YOU

FUEL BUSINESS GROWTH

AUTOMATE VALUE CHAIN

MANAGE WORKFLOWS

Fuel your enterprise growth with Salesflo’s groundbreaking Sales & Distribution software enabling you to manage workflows, generate live insights, and increase sales efficiency with our unparalleled field force performance enhancement ecosystem.

Join Industry Leaders Growing Their Business with Salesflo

Salesflo's Integrated Technology Stack, Your Foundation for Success

Salesflo continues to provide best-in-class solutions in order to help our clients thrive

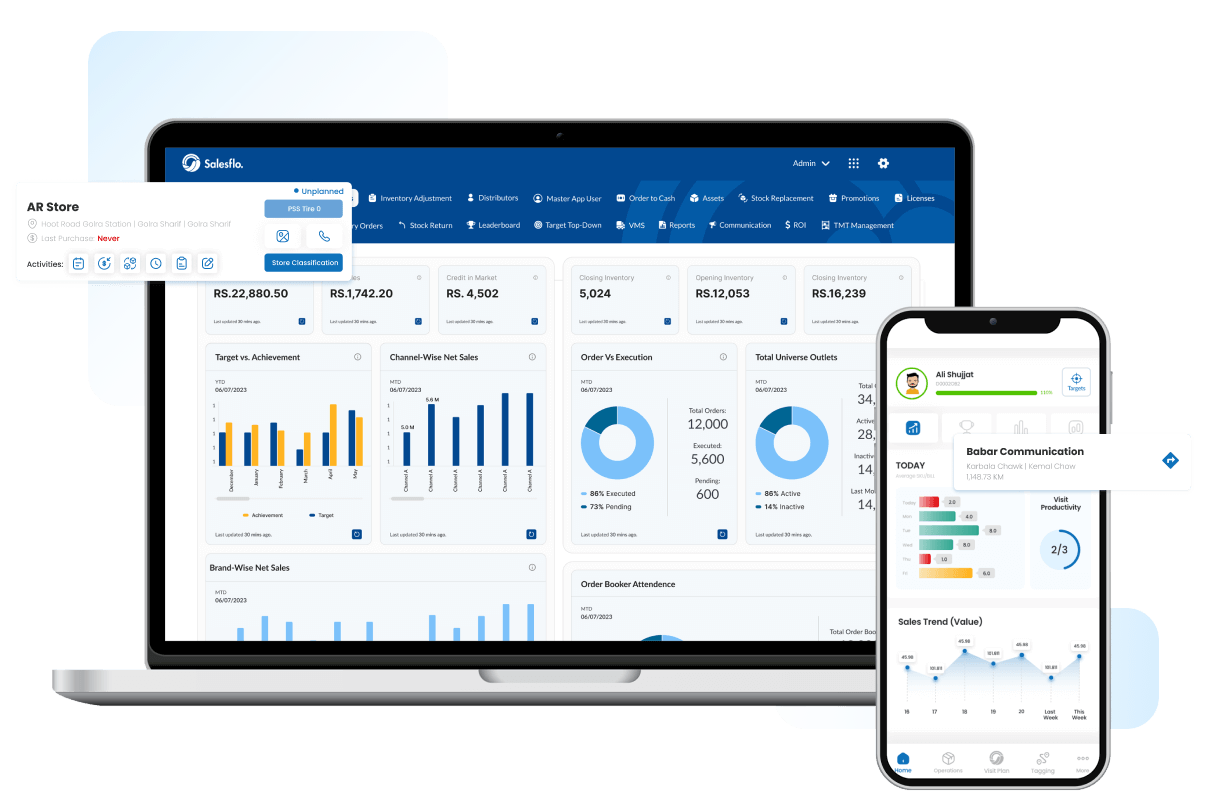

Salesflo Core

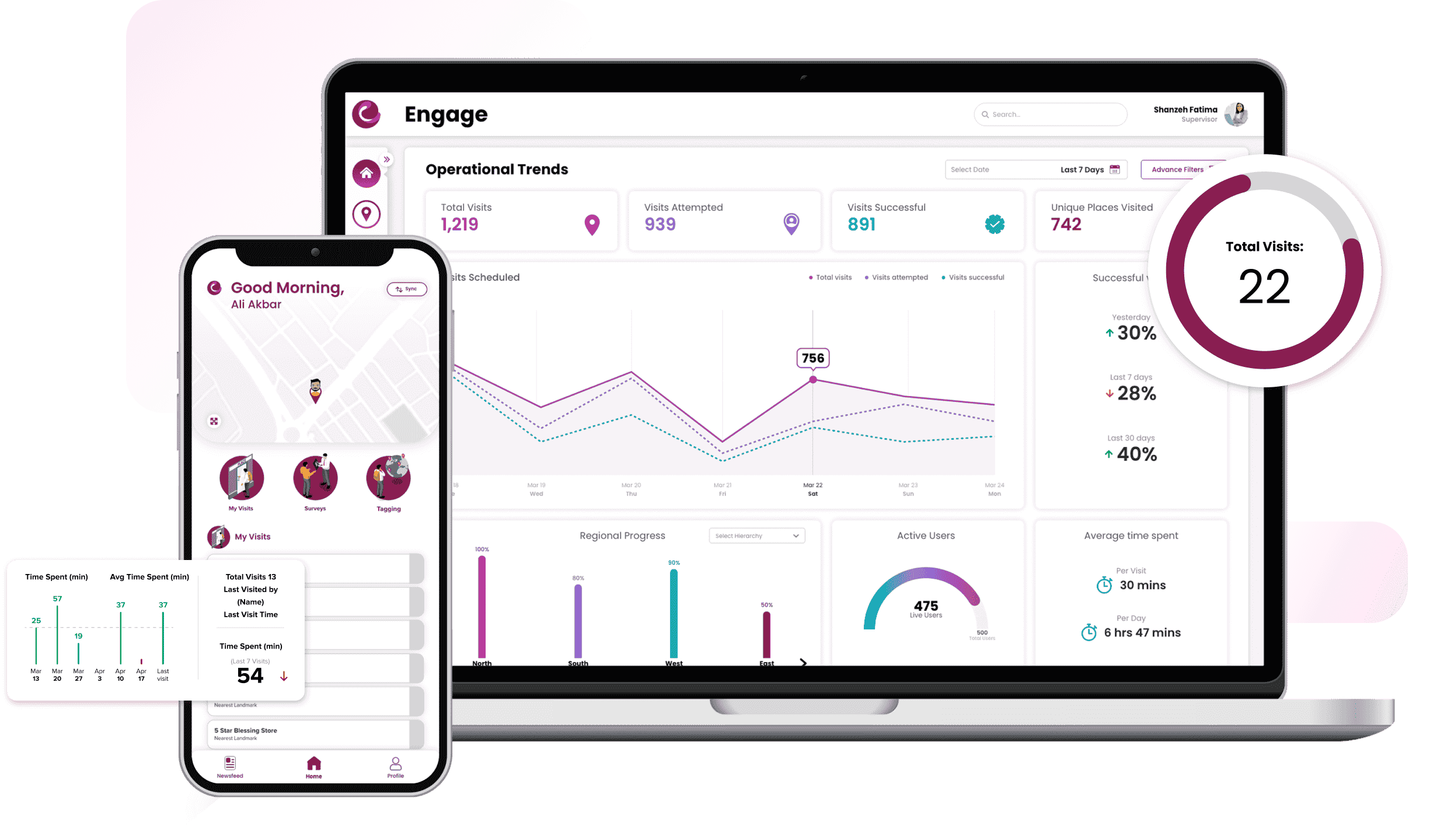

Salesflo Engage

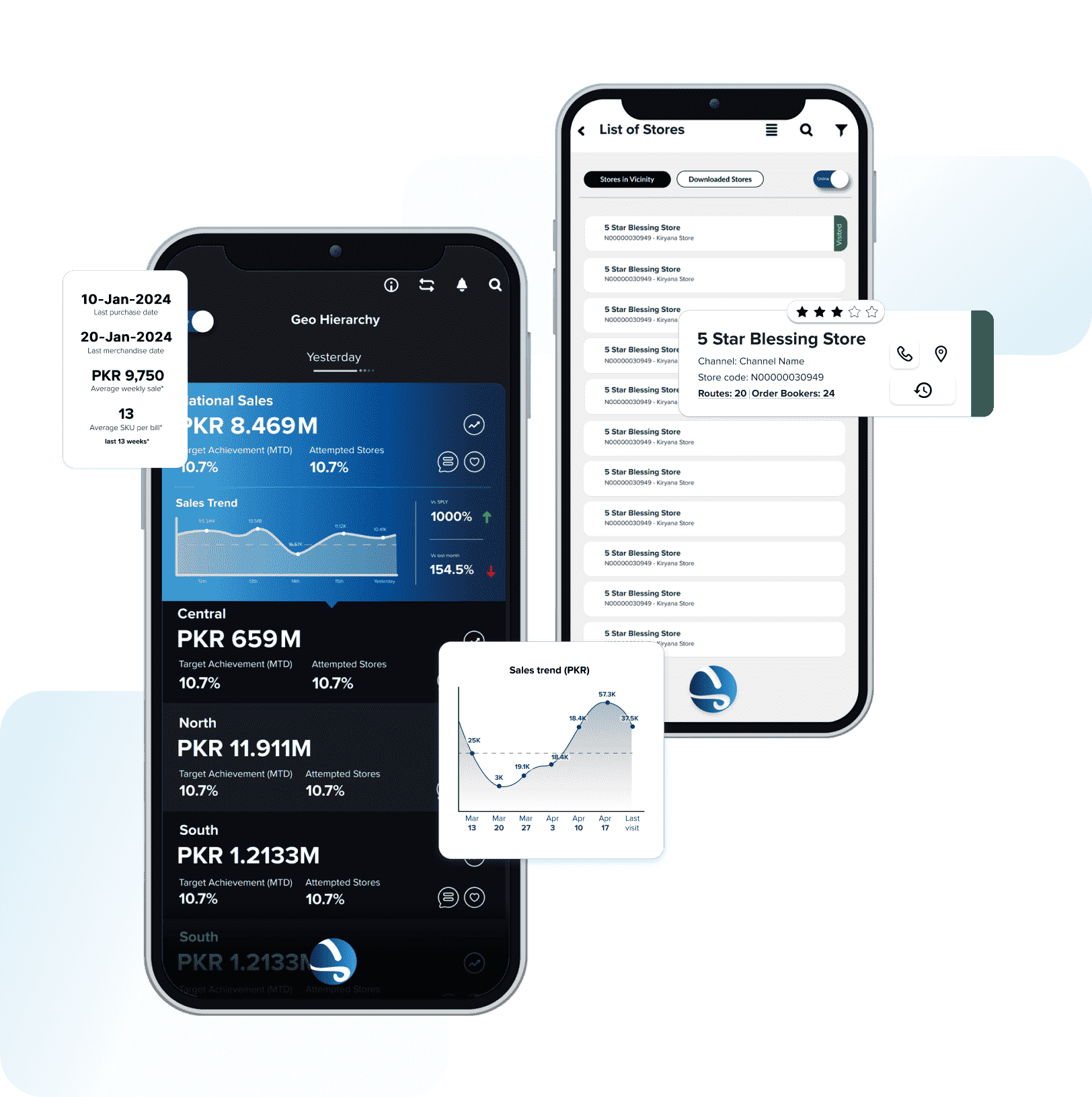

Salesflo Pulse

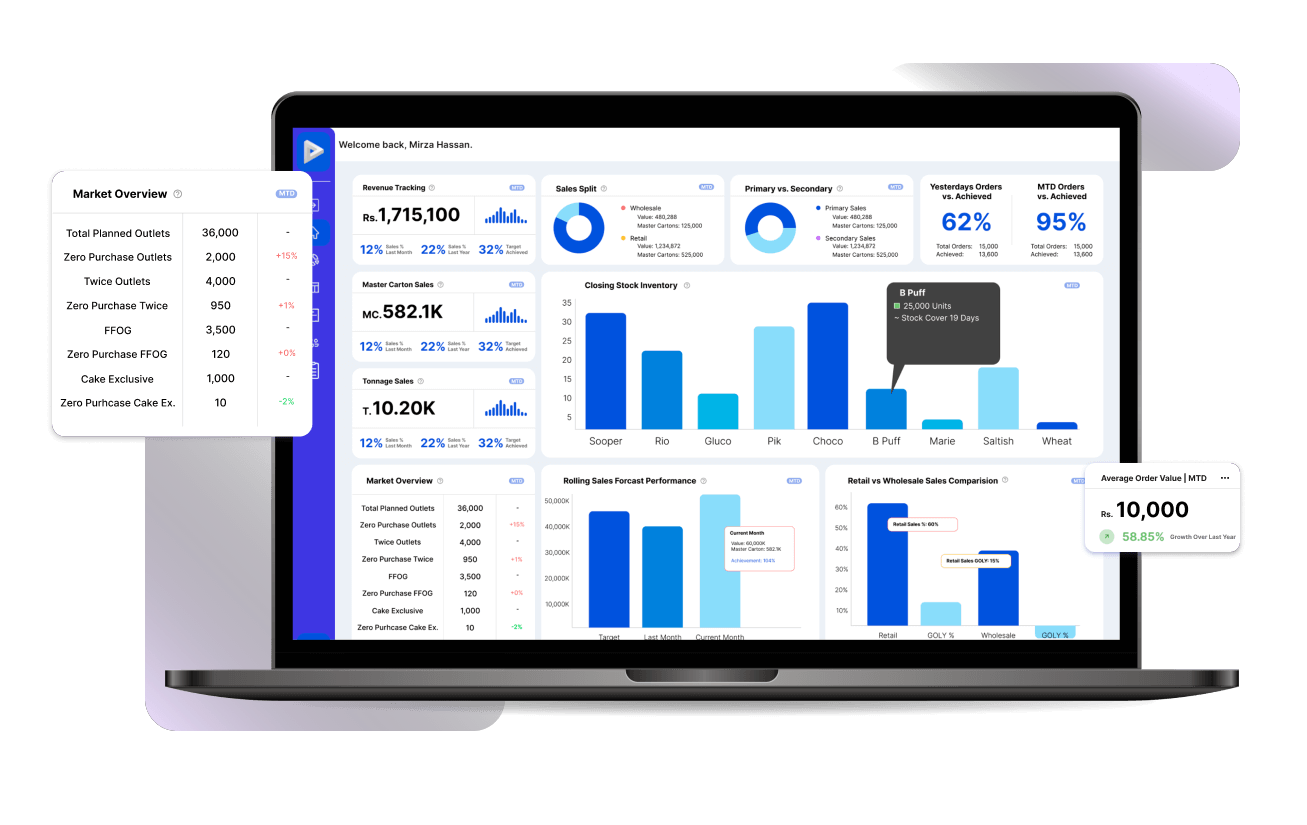

Salesflo Sight

Salesflo Core

An award-winning end-to-end Sales and Distribution management system that helps fuel your business growth and boost Salesforce efficiency by automating the entire Business Value Chain.

Automate business processes/workflows management to track your field operations and collect data to derive actionable insights with our best-in-class Workflow Management Tool.

Salesflo Pulse is a dynamic web-driven Business Intelligence solution, reporting and analytics tool facilitatingthe seamless integration, in-depth analysis, engaging visualization, and effortless sharing of vital data.

Create customized reports, generate insightful dashboards and unlock the power of data on demand, with real-time insights to drive impactful decisions with our next generation reporting and analytics tool.